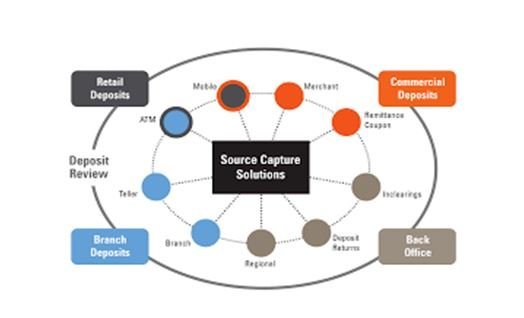

While Remote Deposit Capture (RDC) offers undeniable convenience and efficiency, it also introduces certain vulnerabilities, particularly in terms of money laundering and terrorist financing. Financial institutions must take proactive measures to reduce, if not eliminate, these risks associated with RDC services.

One critical step is for financial institutions to invest in the right enterprise-wide detection technology and integrate methods that thoroughly investigate all channels before processing. By doing so, they can continue to offer RDC while limiting the potential risks of money laundering and terrorist financing. This approach creates a win-win situation for both the financial institutions and their customers.

Additionally, financial institutions can adopt policies, procedures, and controls specific to RDC technology. These policies should outline how transactions are monitored and establish clear limits. Periodic reviews and risk management reports related to Anti-Money Laundering (AML) issues associated with RDC systems and services should be conducted and documented. Strong internal controls and monitoring serve as the first line of defense against the risks associated with RDC, followed by reviewing and investigating accounts across payment services.

Before offering RDC services to a customer, proper Know Your Customer (KYC) and Customer Due Diligence (CDD) review procedures should be undertaken. The RDC service should be classified as high risk, and Enhanced Due Diligence (EDD) should be performed on the customer, with senior management approval required. Financial institutions should develop a detailed Service Level Agreement (SLA) that clearly defines each party's role, responsibilities, and liabilities, as well as record retention procedures for RDC data. The SLA should also establish expectations for physical and logical security in terms of access, transmission, storage, and disposal of original documents.

Furthermore, financial institutions should educate and train their staff on the risks, rules, regulations, and procedures associated with RDC services. They should work collaboratively with customers to help them understand how to protect their accounts and avoid vulnerabilities. Establishing continuous reporting mechanisms to promptly identify and report suspicious activity can also be a crucial step in reducing the impact of RDC vulnerability to money laundering.

In today's competitive financial landscape, institutions that embrace distributed capture options, including RDC capabilities, are positioned to thrive. Failing to do so may result in a decline in market share. By implementing these risk mitigation strategies, financial institutions can confidently offer RDC services while safeguarding against potential threats.

Share:

🏦 From Convenience to Concern: The Rise of Remote Deposit Capture (RDC) and Its Risks

🕊️ Protecting Purpose: Safeguarding NGOs and NPOs from Terrorism and Money Laundering Abuse